Zhao Yanjing

Jointly Appointed Professor at the School of Architecture and Civil Engineering / School of Economics, Xiamen University

Thank you, Professor Mao. After listening to the speeches by the three experts and leaders, a prominent feeling is that current practice has already outpaced academia and theory. The criticism from our colleagues in Guangdong just now was very apt. To turn urban renewal into a theory that can be taught in schools, we need to simplify it into a more general model. Today, I want to use these twenty-odd minutes to make such an attempt—proposing an equilibrium model from a fiscal perspective to provide a general analytical framework for urban village renovation. According to this framework, we divide urban renewal into two main categories: one is large-scale development (complete demolition and reconstruction); the other is autonomous renewal (self-renewal by property owners). We will further analyze which type yields better financial benefits, is more sustainable, and better meets the needs of production and employment.

Two Models of Urban Renewal

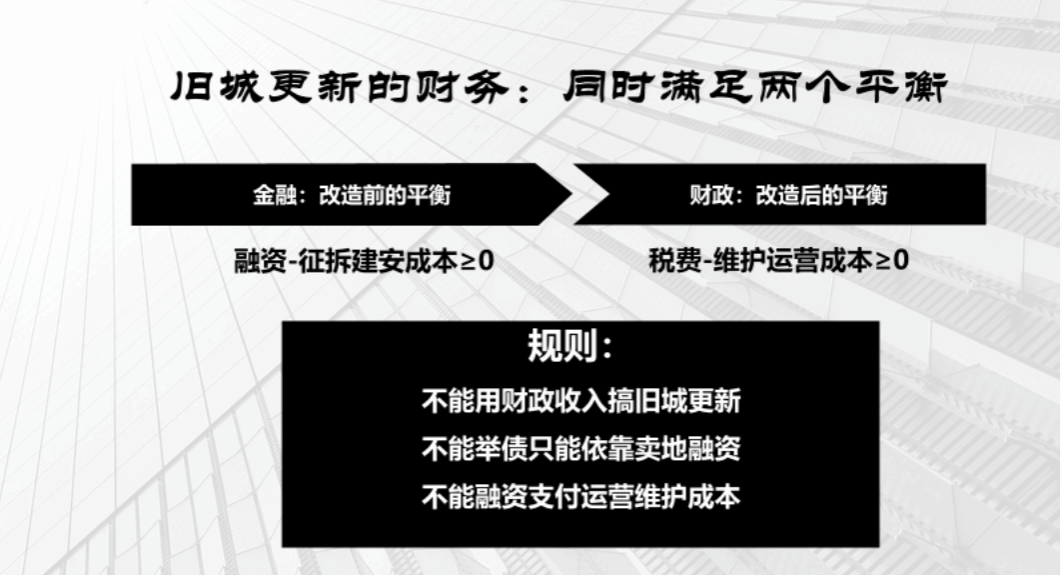

First, our analysis is based on two rules. Rule 1: Fiscal revenue cannot be used for urban renewal; it must rely solely on land sales for financing, so that urban renewal does not lead to a decline in the level of other public services. Rule 2: Financing cannot be used to pay for operation and maintenance (O&M) costs; services must be maintained through general operational revenue, ensuring the financial sustainability of public services. Based on these two rules, all urban renewals must meet two financial balances: 1) At the start of renewal, financing must be no less than the total cost of expropriation, demolition, and resettlement; 2) After completion, the recurring revenue generated must be no less than the cost required to maintain public services without degradation.

There are several premises to these rules. First, when conducting the analysis, fiscal revenue is not used for urban renewal; fiscal revenue is mainly used for urban development and maintenance, such as paying salaries. Our construction should be funded through financing. But the primary financing relies on land financing rather than debt financing. Although local governments are increasingly taking on debt now, this debt is ultimately backed by land, not by mortgaging government tax revenues. Banks lend money not because taxes are high, but because there is land and assets. Therefore, the second rule assumes that most debt is financed directly or indirectly through land. Second, we do not use financing money to support O&M costs. The added supporting services and facilities after completion cannot be covered by land sales or borrowing; the project must have its own "blood-making capacity" (revenue-generating capability).

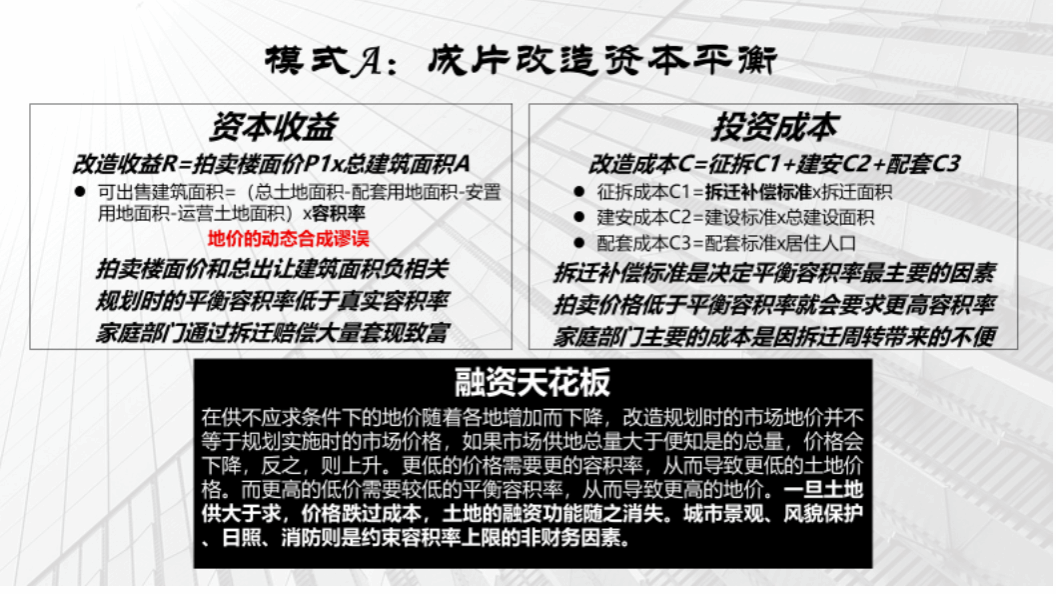

When launching a renewal area, the first step is to see if land sales revenue can balance development expenditures. Factors affecting land sales revenue include the auction price per square meter and the saleable area; their product is the total revenue. The premise for balance is either a sufficiently high land price or a sufficiently high Floor Area Ratio (FAR). Cities with high land prices need a lower FAR to balance; cities with low land prices need to sell more land or have a higher FAR. Major expenditure factors include demolition costs (the largest), construction and installation costs (relatively fixed), and supporting facility costs (schools, new roads, pipelines, etc., to ensure per capita public service levels do not drop with population growth). On the revenue side, land auction price × FAR should exceed the expenditure side to cover these three main costs.

In the absence of a property tax system, operational revenue after renewal mainly comes from recurring sources within the area, such as commercial and industrial taxes, and property rents. The higher the revenue per unit area, the smaller the operational area needed to achieve balance. If revenue is low, a larger proportion of property area is needed to balance operational income. Operational costs stem from services provided to the area's population: education, sanitation, greening, transportation, etc. The most relevant variable affecting public service expenditure is the FAR. A higher FAR means more population and increased supporting services. Increasing the FAR has opposite effects in the construction and operational phases—it increases land revenue during construction but raises O&M costs during operation. The essence of land sales revenue is financing, not profit. On the surface, increasing the FAR seems to increase financing revenue, and theoretically, there is always a FAR that can meet the capital needs of the construction phase. However, the higher the FAR, the larger the gap in operational costs after renewal.

Model 1 is large-scale development—using the market to expropriate land, rebuilding with residents returning, and covering costs through FAR increases. This model essentially relies on land sales for real estate development; otherwise, it cannot balance. The result is inevitably a massive amount of commercial housing rather than affordable housing. Model 2 is autonomous renewal, primarily relying on residents' self-renovation. As colleagues from Guangdong mentioned, owner participation in renovation accounts for a large proportion in Guangzhou, even more than the government. This model does not rely on land financing; investment is mainly borne by owners, with the government primarily providing approval and incentive policies. These two models actually involve two sectors: the government sector and the household/enterprise sector. Different models transfer different amounts of benefits between the two sectors. Different renovation models cause different disturbances to the city's housing supply-demand balance, thereby affecting equilibrium housing prices and FAR. The share of land financing occupied by urban renewal will have a huge impact on the city's future growth.

Model 1: Large-scale Development

The cost of large-scale development is mainly balanced by land sales. Many financial analyses habitually use current market real estate prices as the asset prices after urban renewal, which is a huge misconception. Because once you start dumping assets, market supply and demand will change; the more you dump, the greater the supply, and the lower the price. Therefore, the FAR calculated during planning is only an approximate result under the assumption that the project's urban renewal accounts for a very small share of total market supply. For developers, once all renewed commercial housing is sold together, the estimated sales price at the time of land purchase no longer has reference value.

In this process, demolished residents often receive huge super-normal compensation. The higher the government's compensation standard, the larger the scale of wealth transferred to original residents. The method of transfer is to extract social wealth through FAR increases and then compensate the demolished original residents. On the surface, the government spends no money, just granting a FAR, but actually, increasing the FAR is no different from adding new land supply. Selling land is the government taking on debt, and all FAR increases need to be repaid by providing free public services for the next 70 years. During the construction phase of renewal, expropriation compensation is the most significant factor affecting costs. If compensation standards are high, a very high balancing FAR is required, but financing has a ceiling; it's not that the higher the FAR, the better. Many leaders, developers, and even design institutes have the illusion that money is not a problem in urban renewal, and as long as the planning bureau gives them a FAR, they can definitely balance it. As I mentioned earlier, once market supply increases, the price of the land or houses you sell will also drop. What seems balanced now will not be balanced when everyone sells land together. At this time, a larger area and higher FAR are needed. But a higher FAR will lead to a greater drop in prices. When the price falls below the cost of expropriation, demolition, and resettlement, the land market loses its financing function, and cities will face the distress of being unable to sell land.

Increasing the FAR is not just about destroying the urban fabric and lowering the overall value of the city. On the other hand, many factors prevent cities from increasing the FAR. For example, in landscape-sensitive areas like the surroundings of West Lake or the old city fabric area in Beijing, balance cannot be achieved by increasing the FAR. Additionally, technical reasons such as sunlight access and fire safety also limit FAR increases. Now, professional planning bureaus know that FAR cannot be increased infinitely, but after merging into the Natural Resources departments, most leaders are unfamiliar with planning business, and professional voices disappear in government executive meetings.

If we say that increasing the FAR can achieve financing balance during the construction phase, then in the operational phase after renewal, the FAR becomes the main reason for financial imbalance. This is because the higher the FAR, the more the population, the more public services needed, and the higher the operational costs. If you double the FAR, primary and secondary schools must double, transportation must double, green space must double, water, electricity, and various service facilities must double. Otherwise, urban renewal will not only fail to improve urban public services but will also lead to an absolute decline in per capita levels. In built-up areas where land is extremely precious, it is often impossible to synchronously upgrade these facilities even with money.

China's tax system and capital market structure dictate that local governments must be strong in finance but weak in fiscal revenue. In countries with property taxes, increasing the FAR and property value will bring corresponding tax increases. But in China, FAR increase revenue is a one-time financial gain (land sales). In the operational phase, not only is there no new tax increase, but it also consumes a large amount of fiscal revenue to maintain the increased residential population. Of course, urban renewal can also plan some urban functions that bring taxes. But in reality, because the land prices for such uses are relatively low and they occupy a large area, the construction phase often compresses these functions to achieve financing balance. Therefore, many urban renewal projects end up being almost 100% commercial housing; otherwise, a very high FAR is needed to balance. For projects renewed under the FAR increase model, public services will not only fail to improve but will mostly worsen further. Not only will it fail to achieve the goal of enhancing the city's "appearance," but it will also leave a huge fiscal gap for future city governments.

All financial gains today are future fiscal costs. Good urban renewal must achieve balance in both the construction and operational phases. Large-scale development that relies on FAR increases to cover renewal capital may seem to easily achieve first-stage balance, but it leaves a huge gap for the future. However, because the GDP brought by fixed asset investment in urban renewal is credited to the current government, allowing main leaders to get promoted, many cities are addicted to this renewal model.

Model 2: Urban Autonomous Renewal

"Autonomous renewal" means residents bear the main costs of urban renewal. Since it uses the original residents' own properties, no new land needs to be expropriated, and the main renewal cost is construction and installation. The government has neither investment nor revenue in this process (perhaps the government's benefit is that it "looks good"). The main benefit for residents comes from the asset premium after renewal. For example, a house originally worth 10,000 RMB per square meter appreciates to 15,000 or 20,000 RMB after renewal. The characteristic of this model is that it greatly reduces the government's financing burden.

The first question is whether residents have the intrinsic motivation for autonomous renewal. The answer can be found by looking at the ubiquitous illegal constructions (adding height and width) in cities, which shows the strong demand of residents to upgrade their properties. From the perspective of capital returns, autonomous renewal can transmit the land value appreciation brought by public service improvements to residents' properties. When the original properties were built, construction standards were low, lacking elevators, kitchens, and bathrooms, and the floor price and land price were severely mismatched. After reconstruction, the combination of high-level public services and high-quality properties will inevitably release the land value suppressed by low-grade housing.

The second question is the funding source for residents' autonomous renewal. Most old buildings have limited areas, requiring the government to grant a certain amount of FAR increase to achieve equipment upgrades. For a 60-square-meter apartment, a 10% FAR increase means 6 square meters. Taking Xiamen as an example, housing on the island is mostly over 50,000 RMB per square meter. 6 square meters is equivalent to 300,000 RMB, which is enough to cover all on-site reconstruction construction and installation costs. For a few households that really have no savings, the government can provide full subsidies by holding a portion of the property, recovering the principal when the housing is sold in the future. The government can also sell this option in the market for cash.

For the government, autonomous renewal adopts a non-government-led approach, mobilizing private capital to participate, greatly reducing the government's financing burden. The city can complete the on-site renovation of residents' properties without large-scale FAR increases. Although the GDP brought by fixed asset investment appears to drop on the surface, the cost of residents' autonomous renewal (construction, installation, decoration, updating appliances and furniture, etc.) will significantly drive consumption upgrades. Most importantly, this model will not bring an increase in operational phase costs. Although the FAR reward leads to an increase in total construction area, since the total number of households does not increase, the per capita burden of basic public service facilities will not increase synchronously. The per capita levels of services such as education, sanitation, fire protection, and transportation remain basically unchanged. It will not cause a future fiscal gap for the government, thus achieving financial balance in both the construction and operational phases of urban renewal.

For residents, the renewed housing, due to rising asset prices and increased area, is sufficient to cover all capital expenditures. Since original residents do not need to pay for their own land, as long as policies can solve the matching of usage rights for the newly added area, most residents can afford most of the autonomous renewal costs through installment repayments. If planning control can further enhance the "appearance" of old buildings, it will also bring additional improvements to the overall value of the city and community. Compared with the large-scale development model, although autonomous renewal also requires internal coordination among residents, the construction cycle is often shorter. Multi-story housing can complete construction and decoration within a year. In contrast, large-scale development faces difficulties in expropriation and demolition, complex approvals, and longer design and construction cycles for high-rises. From project initiation to resettlement, it often takes 5 to 6 years, or even longer. For elderly residents in the old city, a shortened usable cycle is equivalent to an increase in implicit costs.

Xiamen once proposed an autonomous renewal plan. Under this plan, the government formulated policies: 1) Allow residents of single multi-family residential buildings in Hubin Yili to autonomously negotiate on-site reconstruction; 2) The government provides support in design, agency construction, property rights reconstruction, and approval. According to estimates by the design department at the time, each household only needed about 250,000 RMB to complete the renewal of the building itself, which most households could afford. Considering the 10% FAR reward given by the government, it was enough to cover most of the renewal costs. The figure below shows the construction and installation costs provided by the construction department for residents to choose from based on different construction standards. Now this renewal model has been replaced by large-scale development, mainly because the ultra-high demolition compensation standards and resettlement areas make residents feel that large-scale development is more profitable for individuals. The government, on the other hand, can expand fixed asset investment to boost current GDP.

Utilization of Land Capital

When evaluating urban renewal, two very important basic issues are often ignored: one is the net capital generation rate, and the other is the scale of urban land financing.

For a city's land financing, one should not just look at how much money was made from land sales, but at the net revenue after deducting expropriation, demolition compensation, and infrastructure supporting costs. In the early days of reform and opening up, although land prices were not as high as now, the net capital income after demolition and infrastructure leveling could reach about 80% of land sales revenue. Now, although land prices are getting higher and higher, about 80% of land sales revenue is used for compensation and supporting facilities. In some urban renewals, even the vast majority of land price income is used to compensate original residents. Only the free capital obtained through financing can bring real growth momentum to the city.

The second is the capacity of the local capital market. Because the total number of houses that can be sold in a city each year is fixed, lowering prices will only affect consumption constrained by finances. Due to lower prices, an increase in quantity does not necessarily lead to an increase in the net capital generation rate. Investment demand is more sensitive to price changes than to the absolute price level. The upper limit of urban housing sales determines the upper limit of the total scale of urban land financing. This means that for any city, the total amount of capital that can be obtained from land within a certain stage is fixed—you cannot obtain an arbitrary amount of capital through unlimited land sales. When the land financing for one project increases, it will actually occupy the financing quota of other projects. Obviously, if a city finances large-scale urban renewal, the capital available for other urban development purposes will decrease. Where limited capital is invested will decisively change the direction of the city's future growth.

A typical example is the urban village renovation in Kunming. In 2008, one month after Qiu He took office in Kunming, 336 urban villages were included in the renovation scope. The method was to give each village "sufficient" FAR to balance the costs of expropriation, demolition, and construction. By March 18, 2015, the number of urban villages included in the planned renovation increased to 382. Of the actually approved 257 urban villages, the approved construction area reached as high as 96.1819 million square meters. Now the urban fabric of Kunming is unbearable; the FAR of hundreds of villages was increased synchronously, destroying the entire city's skyline. A bigger problem with Kunming's urban renewal is that it severely damaged local financing capacity. The area of commercial housing pushed to the market in a short time through old village renovation is equivalent to the total construction area of commercial housing in Kunming's main urban area over ten years. Because urban renewal occupied a large amount of capital, Chenggong New Area, which should have had a higher net capital formation rate, developed slowly instead, causing Kunming to lack sufficient free capital to initiate construction project agendas that bring more cash flow to the city.

Hefei is the opposite example. It did not put the focus of construction on urban renewal with a lower net capital generation rate, but on the primary market with a higher net capital formation rate. It was precisely because Hefei obtained huge free capital in primary markets like Chaohu New Area that it could have classic investment promotion cases like investing in BOE. Modern high-tech industries often require huge capital investments; merely offering preferential land and labor is no longer enough to attract these enterprises. A city's ability to attract investment largely depends on the city's capital investment. Where does this capital come from? Not from fiscal revenue, but from land. Some people online say Hefei took one-third of its fiscal revenue to invest in high-tech industries—this is impossible. A city's capital must come from land financing, either directly (land sales) or indirectly (land mortgage). If the free capital obtained by Hefei in the primary market had been excessively used for urban renewal and public welfare projects, there would be no high-tech city of Hefei today.

Urban Renewal Determines Life and Death

Driving GDP from the consumption side rather than the investment side aligns with the national economic strategic shift from external circulation to internal circulation (dual circulation). Looking at the recovery after the pandemic this year, investment recovery is significantly faster than consumption recovery, and the expansion of investment will inevitably lead to an increase in debt and financing (including land sales) demand. In an economic cycle where corporate revenues and government taxes are shrinking, large-scale urban renewal through land finance will further distort the economic structure and increase financial risks. Autonomous FAR increase does not require land financing, and since original residents receiving FAR rewards are mostly not potential investors in new housing, autonomous renewal will not lead to a drop in housing prices. If planned properly, the improvement in urban architectural appearance brought by urban renewal will even lead to the appreciation of real estate across the city. In the longer term, all our housing today will be dilapidated in the future. If we cannot open up channels for residents' autonomous renewal, relying on large-scale development and land financing for urban renewal is obviously unsustainable.

The examples of Kunming and Hefei show that the current urban renewal model is likely the divergence point for the future great divergence of cities. Whether the urban renewal model adopts comprehensive development or autonomous renewal, the capital consumed and the direction of capital use are completely different. Cities that can create and effectively utilize free capital will enter the fast track of high-quality growth; cities that fail to do so will fall into long-term stagnation or even decline due to debt and fiscal gaps.

Under the pandemic crisis, the capital markets in both China and the US have seen an incredible surge, reflected in the US stock market and the Chinese housing market. Many Chinese cities that were on the verge of collapse in the previous stage suddenly revived, thinking that a new round of capital-driven growth opportunity has come again. Little do they know that this expansion of the capital bubble is the last chance for escape given by heaven! This massive expansion of the capital market is not because corporate revenues have increased or urban efficiency has improved, but the result of national monetary easing under crisis conditions, using national credit to extend the debt of enterprises and governments. If you do not use this opportunity well, do not take the chance to correct the city's balance sheet, but instead think you can spend money freely again, then this round of capital prosperity will not only not be your life-saving elixir, but will become your death warrant. Therefore, if you choose the wrong urban renewal model, you will squander the city's last capital, and you will lose the opportunity to shake off other cities and advance in the high-quality growth competition. You will become a sinner in the history of this city!

Thank you all.

Source: This article is compiled by the Secretariat of the China City 100 Forum based on the speech delivered by Professor Zhao Yanjing of Xiamen University at the Autumn Forum 2020 of the China City 100 Forum, reviewed and published by the author.